TYSONS OFFICE

Corporate Transparency Act Injunction and Exemptions: What the Latest FinCEN Guidance Means for Small Businesses

Jennifer Kim Nguyen

February 26, 2026

If you’ve heard conflicting things about the Corporate Transparency Act (CTA) over the past few years, you’re not alone. The rules have evolved, deadlines have shifted, and recent guidance indicates new Corporate Transparency Act exemptions.

Here’s the headline most small business owners have been waiting for: under the latest FinCEN guidance, most U.S.-formed companies no longer have to file beneficial ownership reports.

Let’s walk through what the CTA is, what changed, who still needs to pay attention, and why this update matters.

A Quick Refresher: What is the Corporate Transparency Act?

The CTA was enacted in 2021 to address concerns about anonymous ownership of U.S. entities. The idea was straightforward: require certain companies to tell the U.S. Financial Crimes Enforcement Network (FinCEN) who actually owns or controls them, so shell companies can’t be used to hide illicit activity.

From the start, the focus was on beneficial ownership information (BOI) — names, identifying details, and control information for the real people behind companies. As the rules were implemented and refined over time, the scope of who needs to report has evolved and narrowed.

What Are the Latest Corporate Transparency Act Exemptions?

As of March 2025, FinCEN significantly narrowed the scope of the CTA through an interim final rule. Under the current framework:

- Entities formed in the United States are exempt from BOI reporting

- U.S. persons are not reported, even if they own a foreign reporting company

- FinCEN has stated it will not enforce BOI penalties against U.S. citizens or U.S.-formed companies while this interim rule is in place

In practical terms, this means that most domestic LLCs, corporations, and similar entities formed in the United States do not currently need to file, update, or correct BOI reports.

For many small business owners, this guidance clarifies what had been an uncertain and evolving compliance landscape, allowing them to focus on their businesses while staying informed about potential future changes.

Who Still Needs to Pay Attention?

While the Corporate Transparency Act’s applicability has been limited, it hasn’t gone away. Instead, FinCEN’s current guidance refocuses the reporting requirements on foreign entities, or companies formed under non-U.S. law that are registered to do business in a U.S. state or tribal jurisdiction.

If a foreign entity doesn’t qualify for an exemption, it may still need to file a beneficial ownership report. Under the current framework, those reports include only non-U.S. person beneficial owners. The CTA’s original 23 statutory exemptions — covering categories like banks, public companies, large operating companies, nonprofits, and other regulated entities — remain relevant, particularly for foreign companies assessing whether reporting applies.

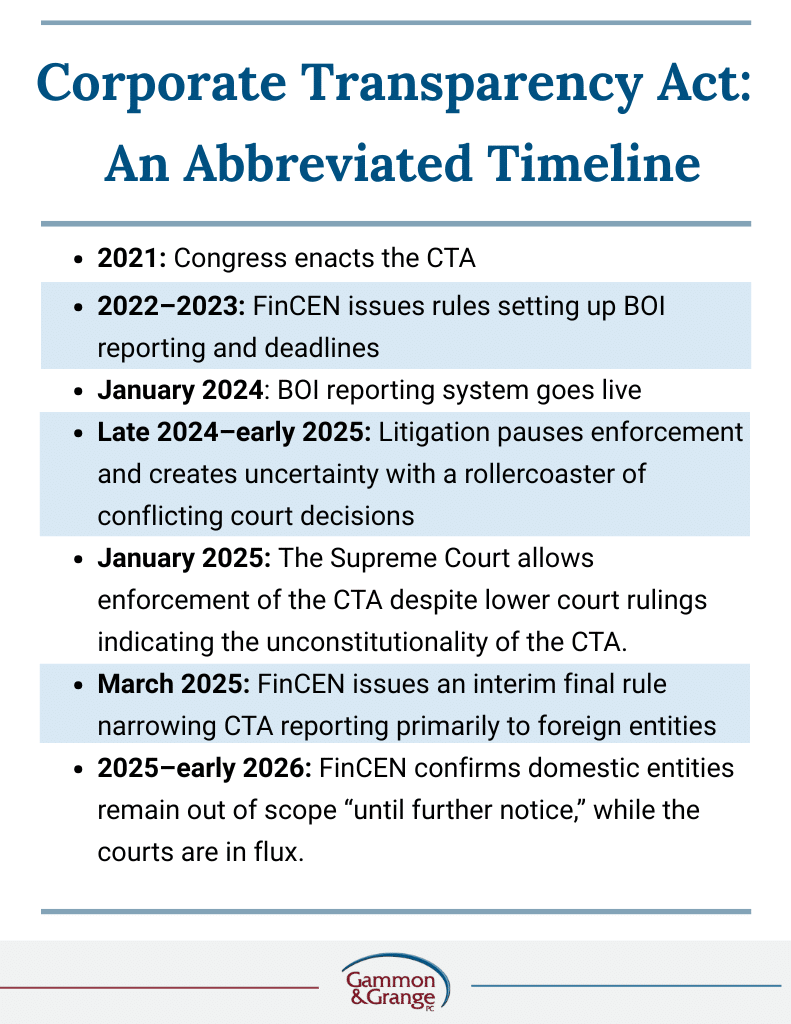

Corporate Transparency Act: The Legal Rollercoaster

If you’re wondering why the rules feel like a bit of a moving target, here’s a quick timeline of how it has evolved over the years:

Why This Still Matters for Small Business Owners

Even under the current exemptions, the CTA remains part of a broader transparency effort combating money laundering and other financial crimes. FinCEN has made clear that it is reassessing how the rules should apply, with an emphasis on higher-risk activity and less burden on typical U.S. small businesses.

For business owners, that means being aware of potential changes to the CTA while having a general understanding of how your entity is treated under federal rules — particularly if your ownership structure changes or involves entities formed outside the U.S.

Key Takeaways

The latest CTA guidance is good news for most small business owners. If your company was formed in the United States, you are likely outside the current BOI reporting regime — and for now, FinCEN has announced it will not enforce penalties against domestic companies while this interim framework remains in place.

That said, the rules have changed before, and they may change again. If you operate through foreign entities, are expanding internationally, or simply want clarity on where you stand, I, Jennifer Nguyen, a small business and estate planning attorney at Gammon & Grange, can help you interpret the latest guidance and plan confidently.

FinCEN Corporate Transparency Act FAQs

Does the Corporate Transparency Act relate to FinCEN’s new real estate reporting rules?

Yes, both aim to combat criminal money laundering issues and illicit financing in the U.S., but they apply differently. The CTA focuses on company ownership, while the new FinCEN real estate news focuses on specific transactions, especially certain all-cash purchases made through entities or trusts. Even if a U.S.-formed entity is exempt from CTA reporting, a non-financed residential real estate transaction may still trigger reporting under the real estate rule.

Who is exempt from the Corporate Transparency Act?

Under FinCEN’s March 26, 2025 interim rule, entities formed in the United States are currently exempt from CTA beneficial ownership reporting. FinCEN has also stated it will not enforce BOI penalties against U.S. citizens or U.S.-formed companies while this interim framework is in place.

Do I need to file a BOI report for my LLC?

In most cases, no. If your LLC was formed in any U.S. state, it is likely exempt from BOI reporting as a domestic entity. CTA reporting is now focused primarily on foreign entities registered to do business in the United States.

Can an LLC have no beneficial owners?

There is usually at least one person who owns a significant share or has substantial control over the business who could be deemed a beneficial owner. However, under the current FinCEN framework, U.S.-formed LLCs typically don’t need to worry about this legal analysis for CTA reporting purposes.

What are the recent court cases and events that have led to the latest changes to the Corporate Transparency Act?

The current CTA guidance from FinCEN has come after some significant rulings and events:

March 1, 2024: In National Small Business United v. Yellen, 721 F.Supp.3d 1260 (2024), the Northern District of Alabama declared the CTA facially unconstitutional, ruling that “it cannot be justified as an exercise of Congress’ enumerated powers.”

December 3, 2024: In Texas Top Cop Shop, Inc. v. Garland, 758 F.Supp.3d 607 (2024), the Eastern District of Texas granted a nationwide preliminary injunction, finding that the CTA likely violated the U.S. Constitution Commerce Clause.

January 7, 2025: In Smith v. United States Department of the Treasury, 761 F.Supp.3d 952 (2025), the court concluded that “the Corporate Transparency Act is unprecedented in its breadth and expands federal power beyond constitutional limits” because it “mandates the disclosure of personal information from millions of private entities while intruding on an area of traditional state concern” and stayed the effective date of the Reporting Rule under the Administrative Procedure Act.

January 23, 2025: In James R. McHenry, III, Acting Attorney General, et al. v. Texas Top Cop Shop, Incorporated et al. on application for stay, the Supreme Court granted a stay for the injunction, allowing for enforcement of the CTA.

March 2, 2025: The Treasury Department announced “not only will it not enforce any penalties or fines associated with the beneficial ownership information reporting rule under the existing regulatory deadlines, but it will further not enforce any penalties or fines against U.S. citizens or domestic reporting companies or their beneficial owners after the forthcoming rule changes take effect [on March 21, 2025] either.”

March 3, 2025: In Small Business Association of Michigan v. Yellen, 769 F.Supp.3d 722 (2025), the court ruled that the CTA’s reporting requirements violated the U.S. Constitution as an “unreasonable search prohibited by the Fourth Amendment.”

March 21, 2025: FinCEN announced on March 26, 2025, interim final rule that suspends enforcement of the CTA against U.S. citizens and domestic reporting companies, acknowledging the widespread judicial challenges to the CTA’s constitutionality.

December 16, 2025: Eleventh Circuit Appeals Court reversed National Small Business United v. U.S. Department of the Treasury, 161 F.4th 1323 (2025) holding that “the CTA is a constitutional exercise of Congress’s power under the Commerce Clause” because “on its face, the CTA regulates activity that is economic in nature” by “effectively prohibiting anonymous corporate dealings, regulating commercial entities that are active in the stream of commerce, and requiring them to report information related to their ownership.”

Current: FinCEN has yet to issue a final rule. In the meantime, the interim final rule remains in effect and is the most current guidance from FinCEN.

This blog provides general information and is for informational purposes only. It is not legal advice, does not create an attorney-client relationship, and should not be relied upon to make decisions about your specific situation. Readers should consult an attorney or other appropriate professional for advice tailored to their particular facts and circumstances.

Share this Article:

Get A Free Consultation

Get a Consultation With a Nationally Recognized Nonprofit And Small Business Lawyer Today.