TYSONS OFFICE

Ranked Last, Acting Fast: How Oklahoma Opted in to the Education Freedom Tax Credit Program

Jennifer Kim Nguyen

May 29, 2026

This post is part of our ongoing series on the Education Freedom Tax Credit — the new federal scholarship tax credit program created under the One Big Beautiful Bill Act. States are opting in one by one, and Oklahoma’s story is one worth telling. If you are new to the topic, we recommend checking out What Is an SGO? for a foundational overview, then reading What Is the New Federal SGO Tax Credit? and How the Federal Scholarship Tax Credit Works.

The One Big Beautiful Bill Act created something that had never existed before at the federal level: a dollar-for-dollar tax credit for individuals who donate to approved Scholarship Granting Organizations (SGOs) that fund scholarships for eligible students. The Education Freedom Tax Credit, also known as the Federal Scholarship Tax Credit, also known as ttakes effect January 1, 2027, and requires states to proactively opt in.

Oklahoma’s path to opting in offers an exemplary roadmap for the states still working through the process or still on the sidelines.

What the Education Freedom Tax Credit Actually Does For Students

At its core, the new federal SGO tax credit is about students and expanding access to educational options for children from families who might not otherwise have them. Donors to approved SGOs receive a dollar-for-dollar federal credit of up to $1,700 per individual donor, and the resulting scholarships can fund tuition, tutoring, textbooks, and more for eligible students, including homeschoolers.

The Oklahoma Council on Public Affairs estimates the program could generate as much as $24 billion in additional education funding annually nationwide — enough to fund private school tuition for 77,000 students or tutoring for more than 300,000 students for every $1 billion in scholarships distributed.

Oklahoma’s Schools and Why This Program Matters

Why this matters in Oklahoma: A recent WalletHub report ranked Oklahoma 50th in the nation in education based on factors like performance, funding, safety, class sizes, and instructor credentials. Furthermore, the 2026 Oklahoma Education Poll found that only 13 percent of Oklahomans give the state an A or B for managing its K-12 system. Dissatisfaction with the state’s education system is bipartisan and widespread.

The Education Freedom Tax Credit offers something the current system hasn’t been able to provide — real alternatives for students and families, funded by private donors, available starting in 2027.

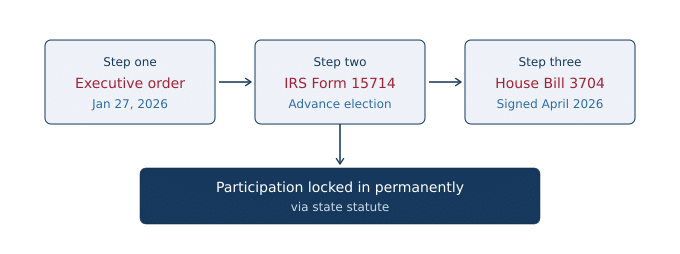

Oklahoma’s Three-Step Path to Participation

Oklahoma’s road to participation in the Education Freedom Tax Credit program is a useful model for understanding how state opt-in actually works in practice. It unfolded in three distinct steps.

Step One: The Executive Order

Oklahoma did not wait for its legislature to act. On January 27, 2026, less than seven months after the federal law was signed, Governor Kevin Stitt issued Executive Order 2026-03. That single action authorized Oklahoma’s participation officially for the 2027 tax year and opened the door for qualifying SGOs operating in Oklahoma to begin the process of becoming officially recognized on the state’s approved SGO list.

The executive order also authorized Oklahoma to coordinate with relevant state agencies to prepare and submit the required list of approved SGOs, setting the administrative machinery in motion well ahead of the program’s effective date.

Step Two: IRS Form 15714

IRS Form 15714 was completed and filed on behalf of the state. This is a new, short form described in IRS Revenue Procedure 2026-6. Making this Advance Election allowed Oklahoma to inform potential SGOs of its participation under section 25F before submitting its SGO list, giving SGOs additional time to prepare for the commencement of this new credit in 2027.

Step Three: House Bill 3704

While the executive order secured Oklahoma’s participation, it left the program’s future dependent on continued executive support. HB 3704, authored by Rep. Denise Crosswhite Hader (R-Piedmont) and carried in the Senate by Sen. Daniels, was designed to fix that by embedding Oklahoma’s participation permanently in state statute. The bill moved quickly, passing the House 73-20 on March 23, clearing the Senate 38-8 on April 15, and signed by Governor Stitt on April 17, 2026.

Under HB 3704, the Oklahoma Tax Commission was designated as the administering agency, responsible for registering eligible SGOs, maintaining the approved list for the U.S. Treasury, and ensuring federal compliance. The bill prohibits state agencies from adopting rules that exceed federal requirements, which keeps the administrative burden on SGOs as light as possible. Oklahoma’s participation is locked in for the long haul — something an executive order alone could never guarantee.

The Federal Credit and Oklahoma’s Existing Scholarship Tax Credit

The Education Freedom Tax Credit offers every individual donor in every participating state the same maximum tax credit benefit. In Oklahoma, this benefit is layered with the state’s existing Equal Opportunity Education Scholarship Act, which provides a state income tax credit of 50% of the donated amount — capped at $1,000 per individual, $2,000 for married filers, or $100,000 for a business entity. The two credits are coordinated: the federal credit is reduced by whatever state credit the donor claims for the same contribution. For an individual donor giving $1,700, the math looks like this:

- Donation amount: $1,700

- Oklahoma state credit (50% of donation): $850

- Federal credit (dollar-for-dollar up to $1700, reduced by state credit): $850

- Combined tax benefit: $1,700

- Net out-of-pocket loss: $0

The $1700 tax offset is the same for participating states. In the case of Oklahoma, however, that credit is reached through a combination of state and federal credits rather than the federal credit alone. The Oklahoma Tax Commission is required to help donors and SGOs understand this interaction so Oklahomans can make the most of both programs.

Where Things Stand and What Comes Next

Oklahoma is one of 29 states that have officially opted into the Education Freedom Tax Credit as of May 2026, with the program set to take effect January 1, 2027. That gives donors, SGOs, and anyone advising them the remainder of this year to get ready. For SGOs, that means ensuring the organization is listed with the Oklahoma Tax Commission before the program goes live. If you are still getting oriented, our post on what an SGO is and how it works covers the fundamentals. A tax attorney can help with organization and compliance.

For donors, getting ready for 2027 really comes down to two things. First, identify a registered Oklahoma SGO you want to support. Second, confirm with a tax attorney or CPA that you have enough federal tax liability to fully use the $1,700 credit. Since the credit is nonrefundable, it can only offset taxes you already owe — it won’t come back to you as a refund if your liability falls short. A brief conversation with a tax professional is all it takes to know whether you are in a position to make the most of this opportunity.

An Example for States Still on the Sidelines

Oklahoma’s proactive three-step approach, executive order followed by statute, offers more than just a window into one state’s process. It is a practical roadmap for any state working to encourage their own state toward participation. For advocacy groups, nonprofit leaders, and mission-driven individuals in states that have not yet opted in, Oklahoma’s story illustrates that a governor can act immediately without waiting for the legislature, and legislation can support and protect this initiative that will benefit the most vulnerable learners. As a result of this proactive approach, will Oklahoma move up in its educational rankings? I am optimistic and hopeful.

As this federal tax credit program continues to unfold state by state, I am following it closely, both as a tax attorney at Gammon & Grange, and as someone who believes in what it is trying to accomplish. If you have questions about how the Education Freedom Tax Credit works, how to create an SGO, or how to optimize your tax strategy, feel free to contact me.

This article is intended for general informational purposes only and does not constitute legal advice. No attorney-client relationship is formed by reading this post. Tax situations vary significantly, and tax law is subject to change. Please consult a qualified tax attorney regarding your specific circumstances.

Share this Article:

Get A Free Consultation

Get a Consultation With a Nationally Recognized Nonprofit And Small Business Lawyer Today.