TYSONS OFFICE

FinCEN Real Estate News: Why the New Residential Reporting Rule Matters in 2026

Jennifer Kim Nguyen

February 19, 2026

If you’re buying or transferring residential property through an LLC or a trust, there’s a new federal reporting rule you’ll want on your radar in 2026. Starting March 1, 2026, the Financial Crimes Enforcement Network (FinCEN), the federal Treasury agency that oversees anti-money-laundering criminal enforcement, is rolling out a nationwide reporting requirement to increase transparency around certain residential real estate purchases.

According to the latest FinCEN real estate news, this rule isn’t about halting entity or trust ownership or restructuring these types of deals. Instead, with the goal of combating money laundering, it changes what information gets reported and at what point in the transaction — especially when there’s no traditional bank involved.

Before getting into who reports and what gets reported, it helps to clarify what qualifies as residential real estate under the rule.

First, the Penalties for Noncompliance

Failing to comply with the Residential Real Estate Rule can carry real consequences. Civil penalties can include fines of up to $1,394 per violation, with higher penalties possible where negligence is involved.

When noncompliance is willful, the stakes are much higher. Criminal penalties can include up to five years in prison and fines of up to $250,000. That’s why it’s wise and prudent to identify potential reporting issues early, rather than discovering them after documents are signed and timelines are tight.

Residential or Not? Why the Number of Units Makes All the Difference

A lot of confusion around this rule comes down to the definition of residential real estate. FinCEN’s definition of residential real estate covers more than just single-family homes. For reporting purposes, FinCEN regards the following as residential property:

- Single-family homes and townhouses

- Condos and co-ops, including units in large buildings

- Any property with one to four residential units

- Certain vacant land meant for residential development

- Mixed-use properties where people live above or alongside a business

If a property has five or more residential units, it generally falls outside the rule. But, if the property does qualify as residential under FinCEN’s rules, the next factor to consider is the financing of the purchase.

How Financing Affects FinCEN Reporting Rules

In many cases, whether or not a particular residential real estate transaction falls under FinCEN’s reporting guidelines comes down to whether or not a bank is involved in the funding of the purchase.

If a qualifying bank is part of the transaction, reporting is usually not required. When, however, the purchase is all-cash or funded through private sources, FinCEN’s reporting rules are much more likely to apply.

Who is Affected by This FinCEN Real Estate Rule News?

Although the rule is focused on reporting, its impact extends across several groups. If you transfer ownership of residential property through an LLC, corporation, or trust, you’ll probably see a few more questions at closing—especially if the deal is all‑cash or uses a private lender instead of a bank. The title or closing team may ask for information about who ultimately owns or controls the entity or trust, and this can come up not only for purchases, but also for certain transfers and even some gifts of property.

On the professional side, attorneys, title companies, and settlement agents play a central role. FinCEN requires that one “reporting person” be responsible for each covered transaction, determined through a reporting cascade or a written designation. In practice, that responsibility often lands with the settlement or title professional involved in the closing.

For people who already use trusts or business entities as part of estate planning or small business ownership, this rule may come as a surprise. In certain non-financed transfers, simply moving a home into or out of an LLC, corporation, or trust may now result in a confidential FinCEN report, even if everything else about the structure stays the same.

Once it’s clear that a transaction may fall under the rule, the next step is understanding what information FinCEN expects to see in the report.

What Information Is Included in a FinCEN Real Estate Report?

When a transaction falls under the rule, one designated “reporting person” must submit a Real Estate Report to FinCEN. The report focuses on identifying the transaction and the people involved, including:

- Who is responsible for filing the report

- Basic information about the property and transfer

- Details about the buyer entity or trust

- Information about the individuals acting on behalf of the buyer

- Beneficial ownership information for the entity or trust

- The purchase price and method of payment

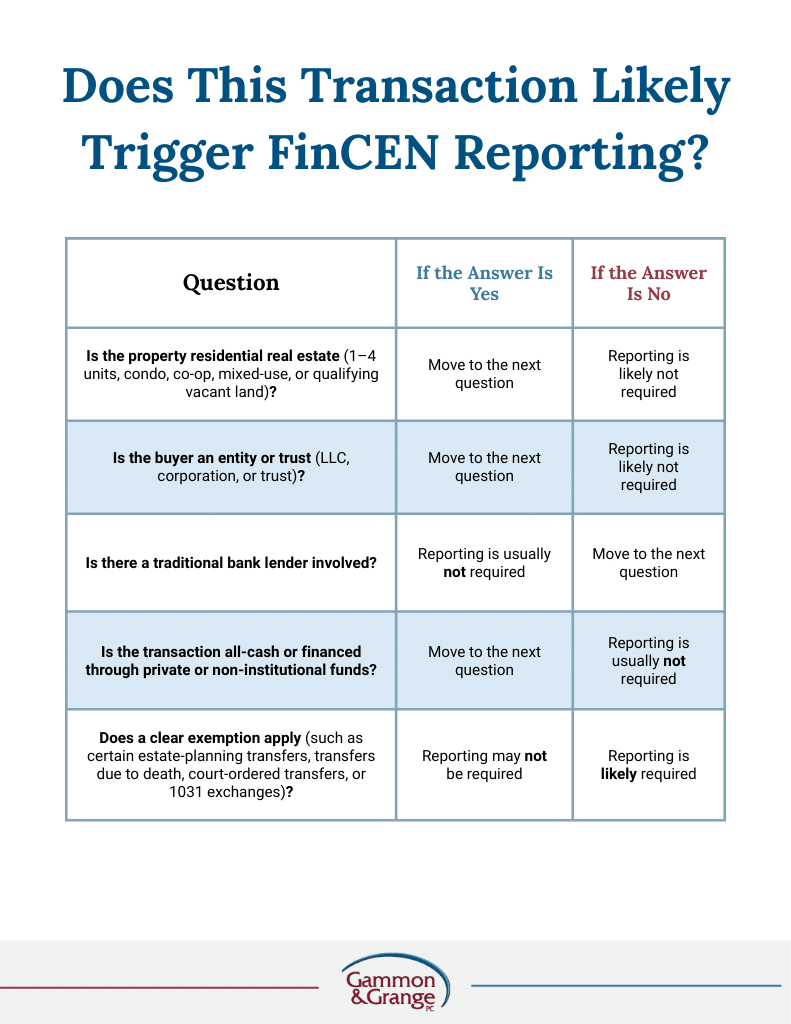

This information is submitted confidentially to FinCEN, and is not made public. Use this table to spot whether a residential real estate transaction may trigger FinCEN’s reporting requirements.

Bottom line: If the property is residential, the buyer is an entity or trust, there is no traditional bank lender involved, and no clear exemption applies, a FinCEN Real Estate Report is likely required.

The Reporting Process

Similar to financial institutions required to file Bank Secrecy Act (BSA) and FBAR reports, reporting persons will file electronically through FinCEN’s free BSA E-Filing System. The Real Estate Report must be filed by the later of (a) the last day of the month following the date the closing occurred; or (b) 30 calendar days after the date of closing through an account. Currently, according to FinCEN, filers may save filings and review whether previously submitted filings were successful, but may not have the ability to access the content of prior filings.

Why These FinCEN Real Estate Rules Matter Now

Whether you’re buying property, advising a client, or handling a closing, the timing of this rule matters. Although it technically took effect in late 2025, FinCEN delayed enforcement, and reporting begins March 1, 2026.

That makes now the right time to prepare. Buyers and investors can avoid last-minute surprises by understanding whether a transaction may be reportable. Attorneys, title companies, and settlement professionals can use this window to update procedures and flag potentially reportable transactions early. Once a deal is scheduled to close, options become far more limited.

FinCEN Residential Real Estate Rule FAQs

How does this rule relate to the Corporate Transparency Act (CTA)?

The Corporate Transparency Act (CTA) requires some companies to report beneficial ownership information to FinCEN when they are formed and when ownership changes.

The Residential Real Estate Rule is similar to the CTA but is triggered by specific real estate transactions, not by entity formation. Filing under one rule does not eliminate obligations under the other. Both reflect FinCEN’s goal of reducing anonymous ownership by collecting new information in different contexts.

Does this apply if I’m buying in my own name?

Generally, no. The rule focuses on purchases by entities and certain trusts.

Are gifts of residential property covered?

Some gifts are exempt, but not all; the details of the transfer matter. Transfers of ownership for which no consideration is exchanged, such as a gift, are reportable.

What about estate planning transfers?

Certain estate-planning-related transfers are excluded, but others may still trigger reporting. According to FinCen, the following transfers of residential real property do not need to be reported:

1. A transfer that is a grant, transfer, or revocation of an easement.

2. A transfer resulting from the death of an individual, whether pursuant to the terms of a will, the terms of a trust (including testamentary trusts), the operation of law (such as transfers resulting from intestate succession, surviving joint owners, and transfer-on-death deeds), or by contractual provision (such as transfers resulting from beneficiary designations).

3. A transfer incident to divorce or dissolution of a marriage or civil union (such as transfers required by a divorce settlement agreement).

4. A transfer made to a bankruptcy estate.

5. A transfer supervised by a court in the United States.

6. A transfer for no consideration made by an individual, either alone or with their spouse, to a trust of which that individual, that individual’s spouse, or both, are the settlors or grantors.

7. A transfer to a qualified intermediary for the purposes of a like-kind exchange for purposes of Section 1031 of the Internal Revenue Code (26 CFR 1.1031(k)-1); or

8. A transfer for which there is no reporting person.

Who files the report?

Only one reporting person files per transaction, determined by FinCEN’s reporting cascade or a written designation agreement.

Will this slow down closings?

It can if reporting requirements aren’t identified early and reporting procedures aren’t put into place.

FinCEN Real Estate News — Closing Thoughts

FinCEN’s new reporting rule reflects a larger shift toward transparency in how U.S. residential real estate is owned — particularly in transactions that don’t involve traditional bank oversight. The intent is to strengthen confidence in the system while still allowing common ownership structures, like LLCs and trusts, to be used appropriately.

Understanding the reporting requirements now can help transactions move forward smoothly and with fewer surprises. For those who regularly use entities or trusts, a small business attorney at Gammon & Grange can help translate these requirements into practical next steps that align with your compliance goals.

This blog provides general information and is for informational purposes only. It is not legal advice, does not create an attorney-client relationship, and should not be relied upon to make decisions about your specific situation. Readers should consult an attorney or other appropriate professional for advice tailored to their particular facts and circumstances.

Share this Article:

Get A Free Consultation

Get a Consultation With a Nationally Recognized Nonprofit And Small Business Lawyer Today.